How to avoid Late VAT registration Penalties?

The UAE Federal Tax Authority must be notified of your liability in undergoing VAT registration when your taxable turnover exceeds the mandatory registration threshold for the past twelve months. The threshold for registration in UAE is currently at AED 375,000.

When the notification regarding your VAT registration in UAE is late and there is no prior notification you’ll be charged regardless of the reason for the delay. A penalty of AED 10,000 will be imposed.

In order to avoid the harsh penalties that are currently in place for late VAT filing or non-filing of VAT, businesses must be wary of all taxation rules and deadlines imposed by the Federal Tax Authority and appoint a responsible person who can accurately record all tax input and output and make filing submissions in a timely manner.

Let MAS handle all your VAT aspects and save your business from unnecessary fines and penalties.

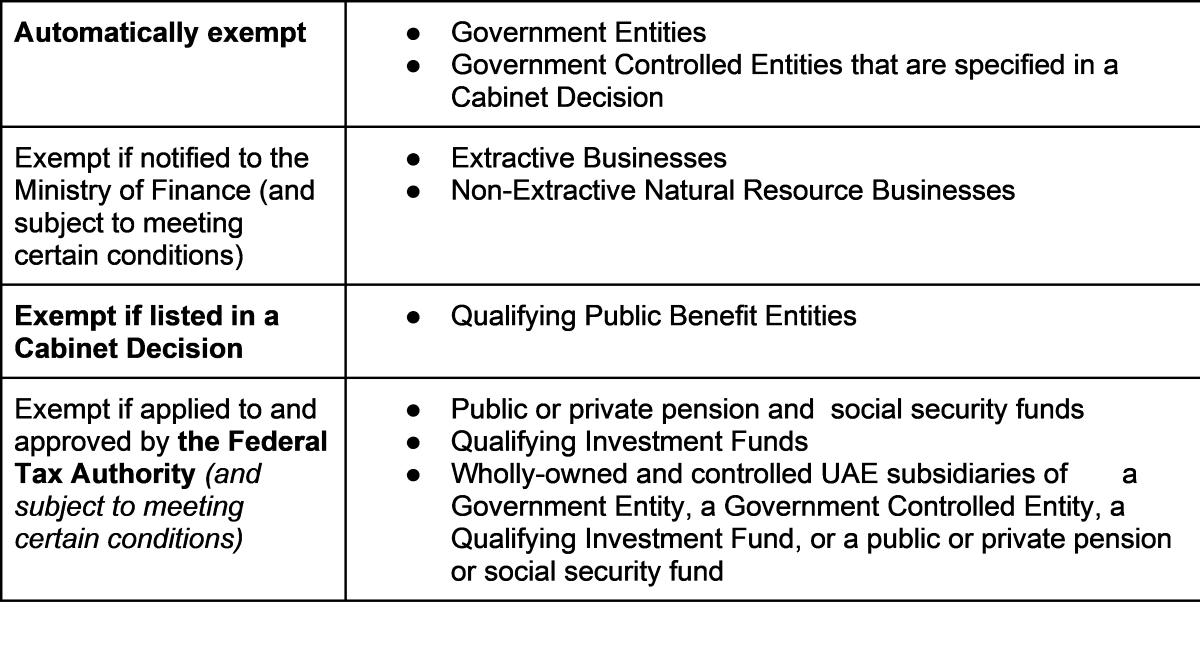

In addition to not being subject to Corporate Tax, Government Entities, Government Controlled Entities that are specified in a Cabinet Decision, Extractive Businesses and Non-Extractive Natural Resource Businesses may also be exempted from any registration, filing and other compliance obligations imposed by the Corporate Tax Law, unless they engage in an activity which is within the charge of Corporate Tax.

In addition to not being subject to Corporate Tax, Government Entities, Government Controlled Entities that are specified in a Cabinet Decision, Extractive Businesses and Non-Extractive Natural Resource Businesses may also be exempted from any registration, filing and other compliance obligations imposed by the Corporate Tax Law, unless they engage in an activity which is within the charge of Corporate Tax.